Depth: Intelligent electric vehicle industry chain research report

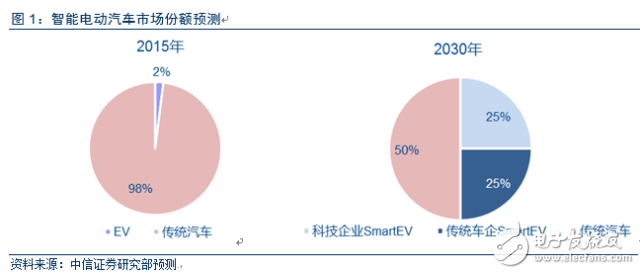

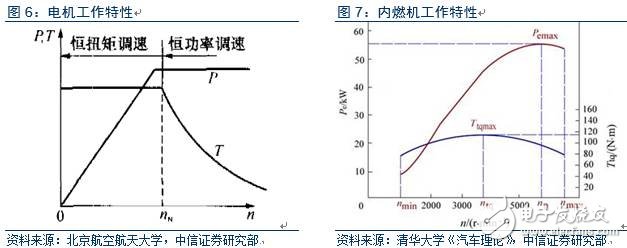

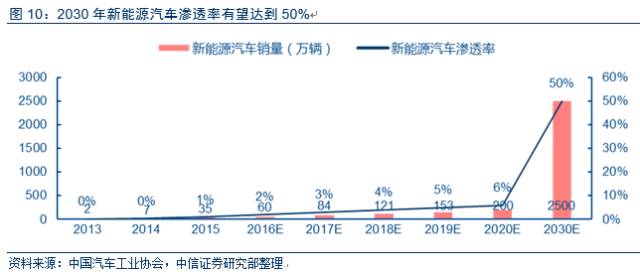

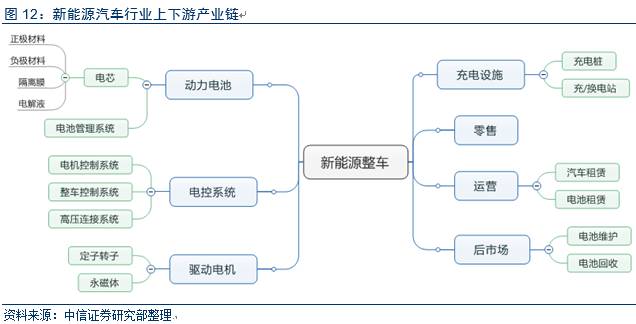

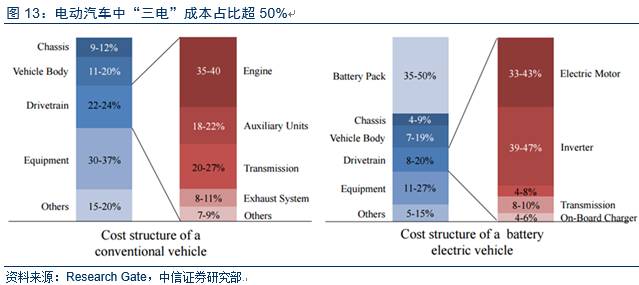

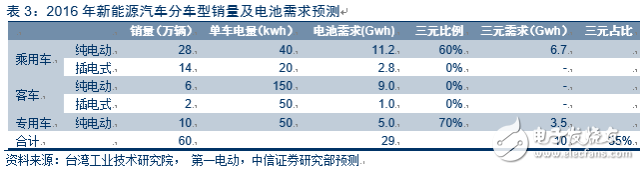

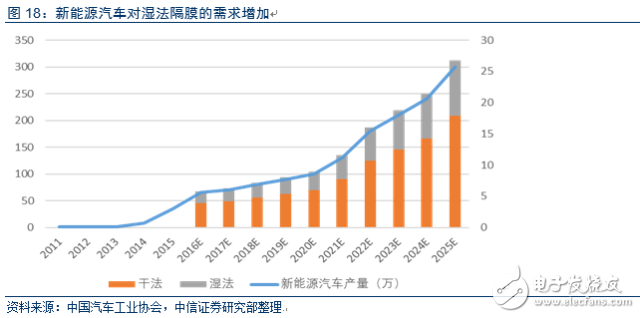

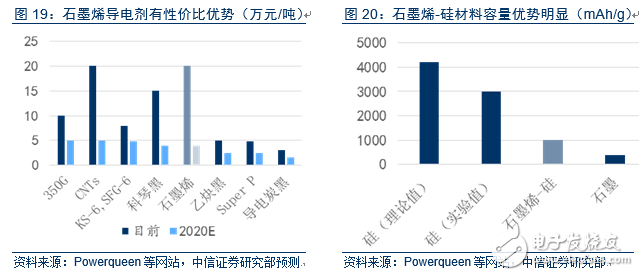

We are in an era of rapid growth in the “slope of technological progressâ€. New technologies and the new business models they generate are emerging one after another. Information technology is advancing by leaps and bounds, colliding rapidly in the cross-cutting field combined with traditional industries and driving many advances. Computers, mobile phones, and TV products have been redefined, and business models such as business and education are also facing challenges. Even in the traditional and heavy automotive industry, it is not difficult to feel the change. The influx of technology companies such as Tesla and Google has intensified the sense of crisis in traditional companies. In the next 10-20 years, automotive products and their industrial chains will face tremendous changes and challenges. “Smart†will be the biggest source of change and opportunity for the automotive industry. One of the focuses of global technology investment will also shift from “smartphone + mobile internet†to “smart electric car + car networkingâ€. “Small, lightweight, intelligent, electric, and shared†will become the core keywords of the automotive industry in the next decade. As consumers become more mature and rational, and energy, transportation, safety and other issues become more and more obvious, the car will eventually return to the essence of smart transportation: "lighter, smarter, safer" will be the future direction. The automobile industry will gradually move from closed to open, from mechanical and electronic control technology to the deep integration of electronics, communication, software, materials and mechanical technology. The automotive industry will become a frontier of innovative technologies across industries and disciplines, and will also stimulate more business model innovation. We expect the market share of smart electric vehicles to exceed 50% by 2030. Among them, emerging car companies may account for half of the country; traditional car companies that have not seized the opportunity for change may become a foundry or even exit the market. In the next five years, technologies such as ADAS and smart driving, car networking, car chips, account numbers and operating systems are worthy of attention. Chinese car companies and entrepreneurial companies benefit from capital strength and engineer dividends, and are expected to undertake more global division of labor in the intelligent process. Electric: Reduce the threshold of building a car and start the prelude of the car's intelligent revolution. Electric vehicles have greatly simplified the structure of automobiles and the number of parts. The core powertrains (such as motors, batteries, and even electronic controls) can be purchased from third parties, thus shaking the system advantages and competitiveness of traditional car companies. Emerging technology-based auto companies have emerged rapidly and hold high-profile "smart" selling points. By 2018, smart cars powered by electric vehicles may once again change consumer perceptions of cars. The battery still accounts for 50% of the current electric vehicle cost. In the future, technologies that help improve battery performance and electric vehicle efficiency are worthy of attention, such as: ternary cathode material, wet diaphragm, graphene conductive solvent, and light weight. Intelligence: Future car owners battlefields from ADAS to driverless. ADAS is an important landing point for smart cars. Foreign giants such as Bosch and China are dominant. The gap between Chinese companies is relatively large. We expect China's ADAS market to reach 200 billion by 2020. With the rapid growth of the market, Chinese companies may seek breakthroughs in the field of post-installation ADAS and early warning ADAS. For listed companies and Chinese startups, the possible opportunities are: 1) automotive chips, 2) electronic brake mechanisms, 3) Laser Radar and millimeter wave radar hardware and algorithms, 4) camera-based and multi-sensor fusion Algorithms, etc. Internet of Vehicles: Intelligent extension and expansion, the rapid development of the rear-mounted car network forced the front loading. The pre-installed car network currently covers a relatively limited business scope, which is common in navigation and basic services, such as General Anjixing. In the future, the front-loading car network may further extend to the V2V and V2X fields, becoming an extension of the sensing mechanism of the ADAS system in special scenarios. Standards such as LET-V are worthy of attention. After the car network is growing rapidly, the industry chain continues to expand, gradually forming a navigation and entertainment-based financial insurance (UBI, etc.), used car service model, also used in automotive loans, car sharing and other fields. In the future, after the car network is based on the "human" life service, it is possible to gradually evolve into a pre-installed business with car operating system and O2O as the carrier. Sharing: Business model innovation based on automotive intelligence. The Internet of Vehicles is the cornerstone of car sharing. Unmanned driving in the future may completely change the car sharing industry. Travel sharing (with drivers) is developing rapidly, vehicle tracking and dispatching algorithms affect customer experience, and capital forces have a greater impact on business models and industrial landscapes. Vehicle sharing (no driver) is based on the vehicle positioning/tracking technology, and C2C mode (such as bump car rental, PP car rental, etc.) is emerging. Capital will play a huge role. The primary market has opened up another round of technology investment boom; the secondary market advantage company is expected to integrate the industrial chain with the financing capability and the status of the listed company, and even form a closed-loop ecological environment. However, it should also be noted that the road to future automobile transformation will be calculated in units of 10 years, which will inevitably accompany the cyclical fluctuations and expected changes in the capital market. The Gartner curve also suggests valuation fluctuations that may result from differences in capital expectations and industrial progress rates. For companies deploying advanced technologies such as smart cars, financing capabilities and cash flow management have become important competitive factors beyond technical strength. The “smart†automotive sector deserves a long-term investment horizon. The “smart†wave of the car in the next decade is worth looking forward to. The car will be led by electronic control technology to the deep integration of electronics, communication, software, materials and mechanical technology, and become the frontier of cross-industry and multi-disciplinary innovation technology. Multi-business model innovation. Electric: lower the threshold of building a car and start the revolution of car intelligence Electric vehicles reduce the threshold of building cars and subvert the core competitiveness of traditional car companies in the field of "powertrain". Electric vehicles have greatly simplified the structure of automobiles and the number of parts. The core powertrains (such as motors, batteries, and even electronic controls) can be purchased from third parties, thus shaking the system advantages and competitiveness of traditional car companies. By 2018, smart cars powered by electric vehicles may once again change consumer perceptions of cars. Electrification is the future direction of development. For individual consumers, high-end electric vehicles can provide strong power and pushback, and low-end electric vehicles can save on gasoline and reduce the cost of using cars. For the country, electric vehicles facilitate centralized discharge treatment and improve efficiency. Technologies that can help improve battery and electric vehicle performance are worthy of attention. The battery still accounts for 50% of the current electric vehicle cost. The problems include: 1) energy density increase and cost reduction, and 2) charging speed increase. Technical directions worthy of attention include: 1) ternary cathode material; 2) wet membrane; 3) graphene conductive solvent. In addition, miniaturization + weight reduction is also a key support for electrification, and carbon fiber and aluminum-magnesium alloys are worthy of attention. 1. New energy opens the smart prologue In the era of electric vehicles, the original core competitiveness of vehicle manufacturers has been shaken, and intelligence will become a core competitiveness. The core competitiveness of traditional car companies in the "powertrain" field has been challenged, and new entrants have played "smart" cards, and cool screens and new technologies have become more attractive to consumers. Tesla opened the prelude to the car intelligence war. Since the start of the booking, Model 3 has accumulated nearly 400,000 orders, and consumers around the world are looking forward to smart and cool black technology. 2. Electricization is the future development trend Electric cars bring a driving experience. The acceleration performance of electric vehicles spikes traditional fuel vehicles. ModelS P90D can achieve a speed of 2.8 seconds per 100 kilometers, setting a world record; BYD "Tang" and "Qin" can easily win the fuel super run. This is determined by the operating characteristics of the motor. Energy conservation and emission reduction are the global development themes. Considering the efficiency of the entire industrial chain from fuel extraction to vehicle-driven Well-to-Wheel, pure electric vehicles are comparable to fuel vehicles, but still have lower energy consumption and emissions than gasoline vehicles. China's oil dependence on foreign countries is high, and electrification is an inevitable choice. According to the statistics of China National Petroleum Corporation Economic and Technological Research Institute, China's current dependence on foreign oil is over 60%, and more than 70% of new oil consumption is car every year. In the long run, the development of fuel vehicles will aggravate China's oil crisis, and electric vehicles will become an inevitable choice. Policies and regulations accelerate the development of China's new energy automobile industry. In 2012, the State Council issued the “Energy Conservation and New Energy Vehicle Industry Development Plan (2012-2020)â€, proposing that the average fuel consumption of passenger vehicles will fall to 6.9 liters/100 kilometers in 2015 and to 5.0 liters/100 kilometers by 2020. . "Made in China 2025" further proposes that the fuel consumption target for passenger cars in 2025 will drop to 4.0 liters/100 kilometers. Regulatory standards have forced passenger car companies to develop electric vehicles. China's new energy auto industry took off quickly with policy support. According to statistics, in 2015, China's new energy vehicle sales reached 379,000 units, a four-fold increase over the same period last year. We believe that China's new energy auto industry has moved toward technological progress with policy support. In 2016, China's new energy vehicle sales are expected to reach 600,000 units, with a penetration rate of 2%; by 2030, new energy sales will reach 25 million units, with a penetration rate of 50%. 3. Future technological progress: power battery technology upgrade New energy vehicles drive the relevant industrial chain. The market size is expected to be close to one trillion in 2020, and the power battery market is expected to reach 100 billion. Power battery is the key link of new energy vehicles. The current industry penetration rate of new energy vehicles is still below 3%, and the high cost of batteries is one of the main reasons for the slow popularity. Pure electric vehicle battery costs account for nearly 50% of the total vehicle cost. The increase in battery energy density, cost reduction, and charging speed are important driving forces for the further popularization of new energy vehicles. The energy density of the ternary positive electrode material battery is 15%-30% higher than that of the lithium iron phosphate battery, and will become the mainstream technical route for the passenger car power battery. The cost of the cathode material accounts for nearly 40% of the lithium battery, which is a key factor in determining the performance of the battery. We expect that the market size of ternary cathode materials in 2020 is expected to exceed 30 billion. We expect that the sales of new energy vehicles will reach 600,000 units in 2016, bringing 10GWh demand for ternary material batteries. Diaphragm is a key component of lithium-ion batteries, and wet-membrane technology will be further popularized. Benefiting from the increase in the penetration rate of ternary and high-end lithium iron phosphate batteries, it is expected that its demand in 2020 is expected to exceed 1.8 billion square meters, and benefit from the continuous gap between domestic supply and demand, product prices and profit margins are stable. The wet diaphragm market is expected to exceed 5 billion in 2020. Graphene or will be used in lithium ion batteries: conductive agents, electrode materials. Graphene is excellent in electrical conductivity and mechanical properties. Currently in the research and development period, it is estimated that the market space will reach 500 million in 2020.

CSRME safety controller is developed for standard GB27607. By monitoring machine tool safety related equipment, the security of machine control system can meet the requirements of GB27607, and its security meets the requirements of ISO13849-1 (PLe) and IEC61508 (SIL3).

With rich interfaces, CSRME has limited programmable function. It can simultaneously replace many different types of safety control modules or safety PLCs, thus greatly simplifying the safety design of machine control systems and reducing cost.

Safety Controller,Modular Safety Controller,Safety Controller,Electrical Safety Controller,Programmable Logic Controller,Banner Safety Controller Jining KeLi Photoelectronic Industrial Co.,Ltd , https://www.sdkelien.com